A Profit and Loss (P&L) statement is a crucial financial document for businesses, offering insights into revenue, expenses, and profitability over a specific period. QuickBooks, a popular accounting software, simplifies the process of generating and managing P&L statements, helping businesses track their financial health.

This blog explores the benefits of using Profit and Loss Statement in QuickBooks, along with step-by-step instructions on setting it up. Whether you’re a new user or looking to optimize your accounting process, this guide will help you navigate QuickBooks’ tools to create accurate, actionable financial reports.

Table of Contents

Introduction to QuickBooks

QuickBooks (QB) is a software that assists businesses with Bookkeeping, Accounting, Payroll, Inventory Management, and other financial processes. You can create financial statements and reports using QuickBooks. Intuit, a California-based corporation, designed QB to help automate common operations, saving time for bookkeeping and paperwork.

For creating charts, business plans, invoices, and spreadsheets, QB provides ready-to-use templates. It can also save time and effort for business owners by automating their signatures on business checks (which are scanned and uploaded for usage). QB also has a lot of advantages in terms of integration with other applications. Learn to set up the QuickBooks Import Excel and CSV Toolkit in the simplest manner possible.

Are you looking for a way to move your QuickBooks data? The easiest and most cost-effective solution is using Hevo, a no-code data pipeline tool. Hevo not only migrates data but also enriches it, making it analysis-ready! Hevo offers:

- More than 150 source connectors from databases, SaaS applications, etc.

- A simple Python-based drag-and-drop data transformation technique that allows you to transform your data for analysis.

- Automatic schema mapping to match the destination schema with the incoming data. You can also choose between Full and Incremental Mapping.

- Proper bandwidth utilization on both the source and destination allows for the real-time transfer of modified data.

- Transparent pricing, with no hidden fees, allows you to budget effectively while scaling your data integration needs.

Thousands of customers trust Hevo for their data integration needs. Join them and experience seamless data migration.

Get Started with Hevo for FreeIntroduction to Profit and Loss Statement in QuickBooks

Quickbooks has 5 major features:

- Cost of Goods Sold (COGS): This refers to the Total Cost Price of the inventory you’ve sold in a specified period of time.

- Revenue: Revenue is the income you’ve earned from selling goods or services.

- Expenses: This is the amount you’ve spent purchasing goods, paying subcontractors, or buying materials for production.

- Gross Profit: Gross Profit is calculated by subtracting your COGS from your monthly revenue.

- Net Profit: Calculate your Net Profit by removing your Expenses from your Gross Profit. Your Net Profit is the exact Profit that your business has made. If your Expenses are higher than your Gross Profit, it means you have incurred a Loss.

Benefits of Using Profit & Loss Statement in QuickBooks

- It allows business owners to develop their reports from the software’s templates instead of creating reports from scratch.

- It is affordable. You can enjoy a wide range of helpful features that QuickBooks offers for as low as $12.50 per month.

- It offers small business owners the ability to expand their enterprise. Many entrepreneurs need loans to grow their businesses. To get a business loan, you may need to provide your Financial Reports to the credit agency or bank.

- It reduces the amount of time a business owner spends on bookkeeping. Profit and Loss Statement in QuickBooks automates the majority of your accounting workload so that you can spend more time on other areas of your business.

- It lets users enjoy a variety of accounting functions on a single platform.

- A Profit and Loss Statement in QuickBooks incorporates your account with payment tools for processes like Inventory Management and Payroll Administration so that you can take care of your Financial Responsibilities in one place.

- Some third-party tools in QuickBooks are PayPal (for Invoice Creation and Online Payments) and Expensify (for Payroll Administration in medium-sized businesses).

Steps to Set Up Profit and Loss Statement in QuickBooks

Follow the steps below to set up a P&L in QuickBooks:

- Step 1: Create a QuickBooks Account

- Step 2: Find the Profit and Loss Statement in QuickBooks Report Center

- Step 3: Choose the Range

- Step 4: Customize your Profit and Loss Statement in QuickBooks

- Step 5: Start Running the P&L in Quickbooks

- Step 6: Print, Email, or Download your Report

Step 1: Create a QuickBooks Account

Click on the ‘Sign Up’ button on the homepage to get started as shown in the image below.

Step 2: Report Center

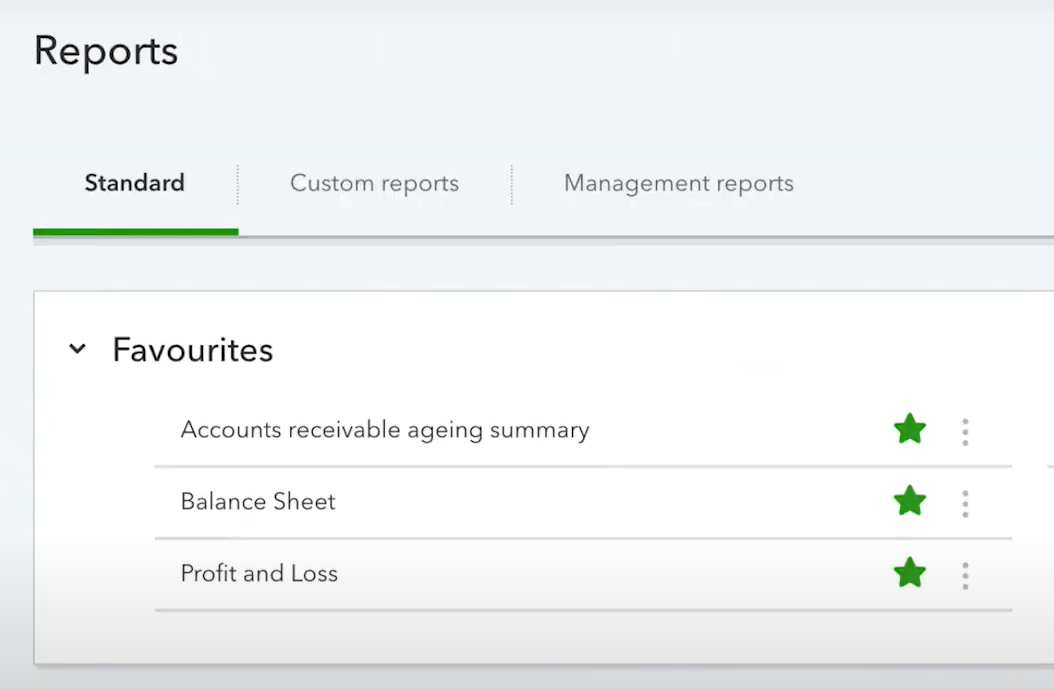

Click on the Menu Bar on the left-hand side of your computer screen, and select ‘Reports’.

Then, click on ‘Company and Financial’. QuickBooks will present you with various options under ‘Company and Financial’. Scroll to ‘Profit and Loss Report Standard’, and click on it.

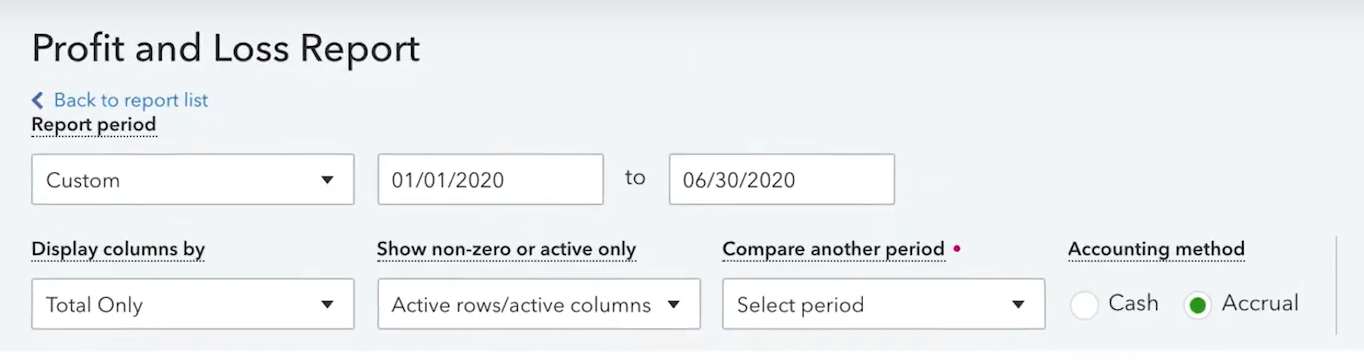

Step 3: Choose the Range

You’ll see a list of options on the top of the Profit and Loss Reports page. Click on ‘Dates’, and select a Date Range as shown in the image below. The Date Range is the length of time you want the report to cover.

Step 4: Customize

The essence of customizing this report is to personalize different options to suit your business needs. Apart from the Reporting Period, you can also customize Columns, Accounting Methods, etc. Set your preferences, and save your changes.

Step 5: Run

Now, click on the ‘Run’ button to finish setting up the Profit and Loss Statement in QuickBooks for your business.

Step 6: Print, Email, or Download your Report

The next step which is the last is to harvest the report by either printing it, sending it to a mail address, or downloading it in the pdf or Excel spreadsheet format.

Conclusion

In conclusion, using the Profit and Loss statement in QuickBooks helps businesses track their financial performance and make informed decisions. By following the simple steps outlined, you can easily generate accurate reports. For seamless data integration across platforms, Hevo is an excellent choice. Hevo’s no-code platform automates your data workflows, ensuring that your financial data from QuickBooks and other tools is synchronized effortlessly for better decision-making.

Sign Up for a 14-day free trial and experience the feature-rich Hevo suite first hand. You can also have a look at the unbeatable pricing that will help you choose the right plan for your business needs.

Frequently Asked Questions

1. What is another name for profit and loss statement in QuickBooks?

Income statement is also called the profit and loss statement.

2. How do I print a profit and loss statement in QuickBooks Desktop?

To print a profit and loss statement in QuickBooks Desktop, users need to open QuickBooks Desktop, go to the “Reports” menu, select “Company & Financial,” and then choose “Profit & Loss Standard.” Then click the “Print” button.

3. Can QuickBooks generate a profit and loss statement?

Yes, QuickBooks can generate a profit and loss statement. Users can access it by going to the “Reports” section, selecting “Profit and Loss,” and customizing the report as needed.

Share it with your connections.

-

Share To LinkedIn

Share To LinkedIn

-

Share To Facebook

Share To Facebook

-

Share To X

Share To X

-

Copy Link

Copy Link